Most people don’t realise how much money they quietly lose on car insurance every single year — without doing anything wrong. You buy the car. You insure it. You renew when the email comes in. And just like that, your premium creeps up.

This quietly costs people hundreds because modern insurers don’t just price accidents anymore. They price behaviour.

If you look predictable, passive, or unlikely to switch, you don’t just become a low-risk driver. You become a high-margin customer.

Here’s what most drivers around the world never hear:

Two people with identical cars, locations, and driving records can pay very different prices — not because one is riskier, but because one looks easier to monetise.

The worst part? You don’t need to change your car to cut your insurance. In many cases, people slash premiums simply by changing how they interact with the system — not by lying, not by cutting cover — but by avoiding the signals that tell insurers they can quietly raise prices.

This isn’t about gaming insurance.

It’s about understanding that you’re not just insured.

You’re modelled.

The Universal Truth: You’re in a Pricing System, Not Just a Policy

Across most insurance markets, pricing engines continuously estimate three things:

- How risky you are

- How profitable you are

- How likely you are to switch

Risk is only one of those.

The uncomfortable reality worldwide:

Two identical drivers can be priced differently because one looks easier to keep — and therefore easier to monetise.

This is not unique to one country.

It’s a standard feature of modern data-driven insurance pricing.

Underwriting Appetite (Why One Insurer Is Cheap This Year and Expensive Next Year)

Insurers manage their books like portfolios.

At different times, they:

- Want more drivers in certain regions

- Want fewer drivers in certain car types

- Want to reduce exposure in certain risk bands

- Shift capital between categories

So pricing changes not just because you changed —

but because the insurer’s appetite changed.

That’s why:

- One company is suddenly cheap for you

- Then suddenly expensive

- With no obvious explanation

You didn’t change.

Their portfolio strategy did.

Profitability vs Risk (A Global Reality)

Modern insurers don’t only ask:

“How likely is this driver to claim?”

They also ask:

“How profitable is this customer likely to be over time?”

They estimate:

- Renewal likelihood

- Price sensitivity

- Complaint behaviour

- Switching behaviour

- Lifetime value

Drivers who look:

- Predictable

- Passive

- Low-switching

often get treated as stable revenue — even if their risk is average.

That’s why loyalty often costs more in practice, worldwide.

Quote Timing (Why Early Shopping Works in Many Markets)

Across many markets, insurers release more competitive pricing during certain windows before renewal.

Early shoppers:

- Look price-sensitive

- Look organised

- Look likely to switch

Late shoppers:

- Look trapped

- Look less mobile

- Look less price-sensitive

This affects how aggressively insurers compete for you — even when risk is identical.

Why Using Multiple Comparison Platforms Matters Everywhere

Comparison sites do not show “the market.”

They show:

- Their partners

- Their commission priorities

- Their exclusive deals

Different platforms surface different insurers.

Using only one means you are seeing a filtered version of reality — not necessarily the cheapest version.

This is true in:

- North America

- Europe

- Australia & NZ

- Many Asian markets

Job Titles, Risk Clusters, and Socio-Risk (Global Pattern)

In many countries, job titles act as proxies for:

- Income stability

- Claim frequency

- Fraud risk

- Stress correlation

- Historical claim behaviour

You are not priced as a unique individual.

You are priced as part of a statistical group.

Choosing the closest accurate category can move you between groups — which can change pricing even if your actual driving is the same.

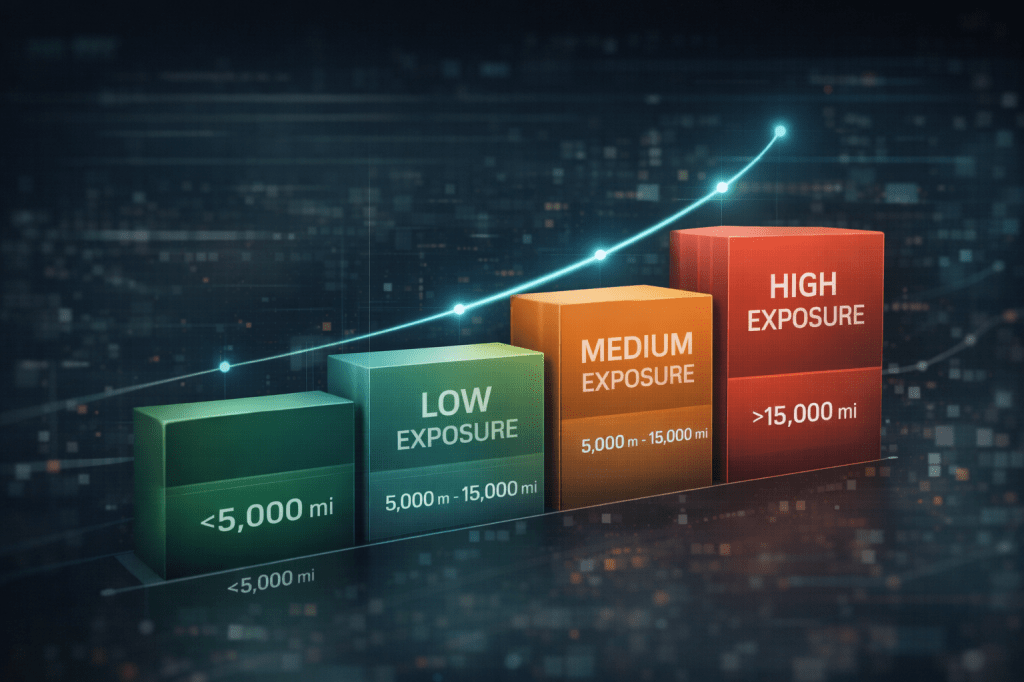

Mileage, Usage, and Tiering (Not Linear, Almost Everywhere)

Most insurers use mileage or usage to classify drivers into tiers:

- Low exposure

- Moderate exposure

- High exposure

- Business-like use

Pricing jumps often happen at tier boundaries.

Small mileage changes can trigger big pricing changes because you’ve crossed into a new category — not because of the extra distance itself.

Excess / Deductible as Behaviour Signal (Worldwide)

Higher excess or deductible does more than reduce payouts.

It signals:

- Lower small-claim behaviour

- Higher friction before claiming

- Lower administrative cost

This changes how insurers forecast claim behaviour — and how aggressively they price you.

Household & Multi-Driver Modelling

In many systems, insurers look beyond just the main driver.

They model:

- Household stability

- Combined driver behaviour

- Shared risk indicators

Adding a low-risk driver can sometimes improve the overall household risk forecast.

The Biggest Silent Cost Worldwide: Looking Predictable

Across markets, the most expensive long-term trait is not risk.

It’s predictability.

Predictable customers:

- Renew automatically

- Shop late

- Rarely compare

- Accept gradual increases

That makes them easier to monetise.

Doing nothing is not neutral.

It actively moves you into a more profitable customer category.

Tools & Services

Comparison Platforms

These are leverage tools, not just shopping tools.

They expose:

- Market variation

- Appetite differences

- Channel-specific pricing

Brokers / Agents

Brokers and agents can access insurers and pricing paths that online tools may not — especially for non-standard profiles.

Telematics / Usage-Based Insurance

In many countries, telematics can replace assumptions with real driving behaviour — often lowering inflated risk estimates.

Renewal Tracking & Reminders

These prevent inertia and stop you from becoming a passive, high-margin customer.

The Real Global Strategy

The goal is not just to lower this year’s premium.

The goal is to avoid becoming a high-margin profile in any market.

Every year you:

- Shop early

- Compare widely

- Refresh your profile

- Avoid automatic renewal

You’re not just saving money.

You’re training the system to treat you as:

- Price-sensitive

- Switch-capable

- Low tolerance for drift

That affects how you’re priced over time — worldwide.

Quick Checklist

- Start quotes early

- Use more than one comparison platform

- Re-enter details fresh

- Review job title / occupation category

- Check mileage or usage tier

- Adjust excess / deductible

- Add low-risk household drivers

- Review parking / storage description

- Avoid automatic renewal without checking

The Universal Takeaway

Insurance looks like a product.

In reality, it’s a system that prices:

- Risk

- Behaviour

- Profitability

- Switching likelihood

- Portfolio needs

Most drivers only think about risk.

That’s why most drivers overpay.

Once you understand the system, you stop being quietly optimised for profit — no matter what country you live in.

Why This Is Effectively the Global Ceiling

At this point, you are explaining:

- Portfolio strategy

- Behavioural pricing

- Lifetime value logic

- Market fragmentation

- Tier-based classification

- Household modelling

That’s about as deep as you can go globally without:

- Making unverifiable claims

- Becoming technical actuarial content

- Creating legal or regulatory risk

- Reducing readability and RPM

This is now not just helpful.

It’s structural understanding.

Which is what actually changes behaviour — and builds authority at scale.

Leave a comment